Are you in the mood for a case study resource for your own investment policy manual? If so, brace yourself because this one is heartbreaking. You can learn a lot from it, and save your own family a great deal of tragedy, but it’s going to involve surveying the ruins of the lives of others so you might want to steel yourself.

I found it courtesy of one of you – thanks Andrew! – who sent this to me in the contact form. I happened to see it while following up on a promise I made to a few of you to check if your messages were getting through (I’m still working on that, an update later). It’s incredible both from a practical, financial standpoint, and a human psychology standpoint. The night I followed the link, I spent the entire evening going through the 535 or so pages, mesmerized by the delusion. It’s a living, breathing embodiment of the opposite of everything I write about in terms of risk management, capital allocation, tax-efficient compounding, and fundamental analysis. It is a testament to the power of temptation, and proves that individual investors, including those who are poor, are frequently just as greedy, and no more moral, than the most avaricious investment banker so demonized in the popular culture over the past few years.

Before we get into studying it, and I publish the link for you to begin your own case study, I have a request: Please do not go onto that forum and comment. Look, but don’t touch. The people in there have lost huge amounts of money, in some cases, their entire life savings. While we can do a post-mortem analysis for our own purposes, causing them to feel more regret is not only cruel, it is unlikely to do any good considering they just learned the most painful lesson of all.

Ready? Let’s dive into this.

The GT Advanced Technologies Bankruptcy

The forum in question was for “investors” – and I do not use the Benjamin Graham definition of that word in this case – in a company called GT Advanced Technologies. GTAT was supposed to be the primary supplier of sapphire glass to Apple, which everyone thought was going to include it on the iPhone 6 and iPhone 6 Plus. Plans changed as GTAT management was unable to execute on time, so the sapphire glass, instead, was going to be used on the upcoming Apple Watch and then in later generations of the iPhone.

What should have been a small bump in the road lead to a shocking, out-of-the-blue Chapter 11 bankruptcy filing and the near total decimation of the common stock with practically no warning. The company had a positive net worth, hundreds of millions in cash at the last quarterly filing, a good probability of making a lot of money in the future, and management reiterating earnings guidance only a few weeks ago.

How could such a thing happen? It was a Lehman Brothers / AIG mistake. GTAT management had not only made poor capital structure choices, it had signed legal agreements that required it to come up with huge amounts of liquidity on little to no notice under the wrong circumstances. Primarily, they funded long-term operations with short-term capital, negotiating a nine-figure, multiple-installment working capital loan from their most important customer, Apple, and then gave Apple the right to demand accelerated payment at virtually any time. Even issuing zero coupon junk bonds on a long-term basis would have been preferable to such a make-it-or-break-it contract.

There were several warning signs that should have been visible to anyone familiar with forensic accounting or basic security analysis. There was an over-reliance upon a single vendor, which requires a huge discount to intrinsic value to justify in most cases if you are going after risk-adjusted returns as you are inherently dependent upon the financial health, goodwill, and continued support of an entirely separate firm. The auditors warned shareholders in the SEC filings of a material deficiency in the internal accounting records, which is one of the handful of things that will make me walk away from a company no matter how good everything else appears (if you can’t trust the numbers, you can’t value the firm). There was a note in the SEC disclosures that the financing arrangement could make it impossible to continue as a “going concern” due to a cash short-fall (if you ever see those words, your eyebrows should shoot up). There were no major contingency plans or back-up capital sources available if the iPhone 6 and iPhone 6 Plus launches were missed. The CEO allegedly had a history of what seems to be a near megalomaniacal desire to swing-for-the-fences, already having run one business into the ground. Apple had no minimum purchase commitments, and no exclusivity contract, so demand projections were entirely speculative.

Given the capital structure and lack of purchase commitments, under no circumstances could a position in GTAT be considered an investment operation as defined in Security Analysis or The Intelligent Investor. It was a speculation and, to be frank about it, not a terrible one. This was a case of the right idea being in the wrong hands. Had management been less reckless, a lot of people could have ended up obscenely rich. Were one inclined to gamble, there were worse ways to do it. It just didn’t work out this time. However, this forum is full of people who didn’t make the distinction. Every imaginable portfolio error can be found in its pages. People taking speculative positions in tax-sheltered accounts (almost always a bad idea as you lose the huge benefit of tax loss credits that would make recovering much easier in the future); buying stock on margin; risking more than they can afford to lose in the event of a total-wipeout; not keeping certain types of capital piles, such as college savings, exclusively in investment operations.

When Andrew sent me this link, he first pointed to this page, about a month before the bankruptcy announcement, when people were talking about how foolish it would be for them to own index funds or invest in a traditional sense. Then, he points to this page, on the morning they realize the stock isn’t trading. You follow their reaction upon discovering the shares have been halted. That bankruptcy has been declared. That the conference call they were expecting had been cancelled. Between it (page 499) and the end of the forum (535 when I read it), you see all five stages of loss and grief – denial, anger, bargaining, depression, and acceptance.

Some Excerpts on the GT Advanced Technologies Forum That Stand Out for the Lessons They Can Teach Investors

Here are a few excerpts, among many, that caught my eye …

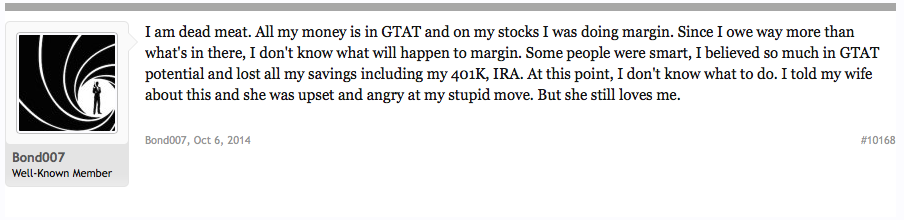

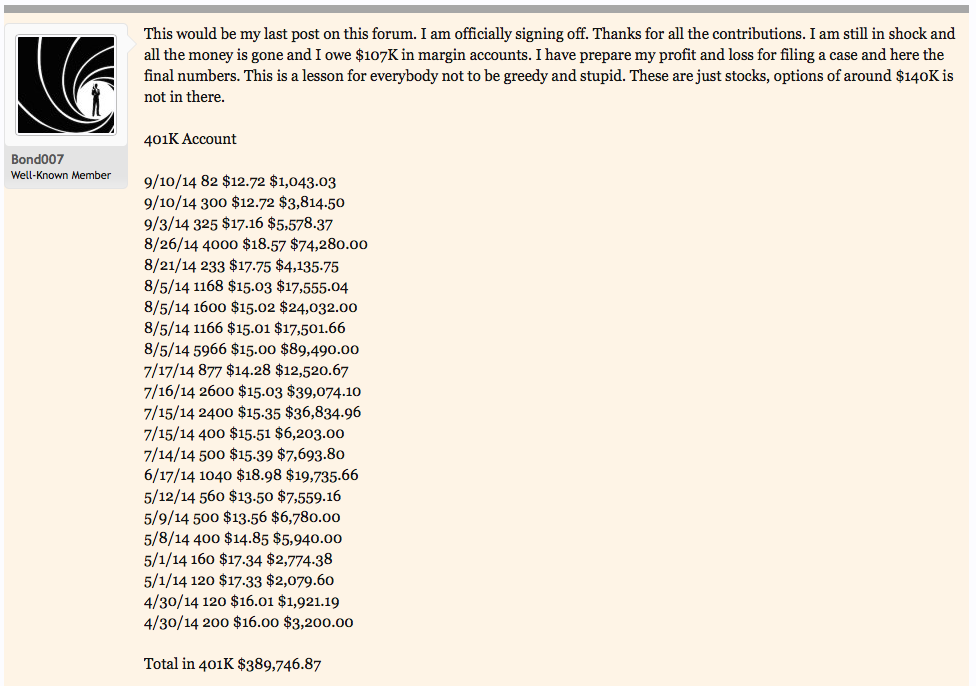

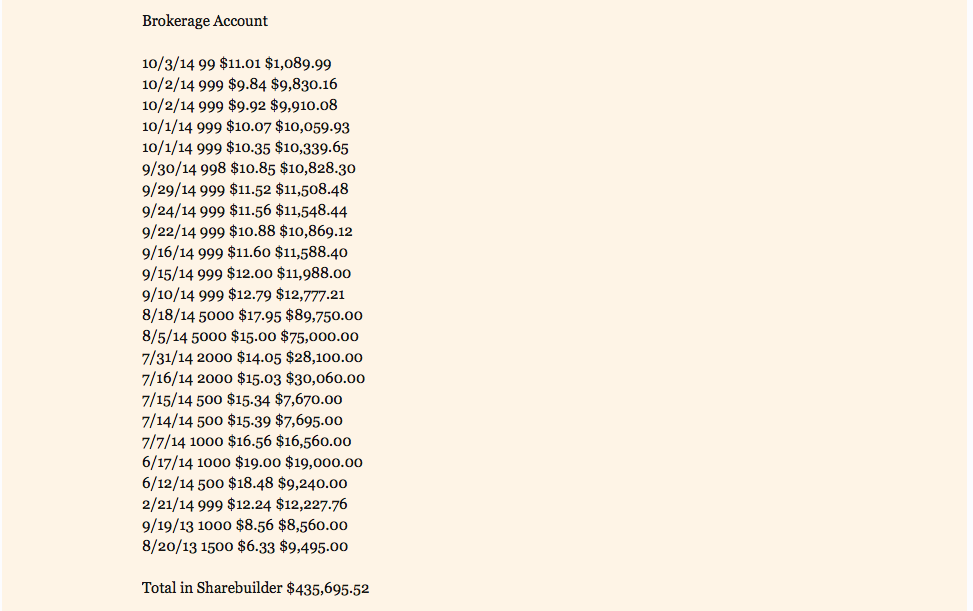

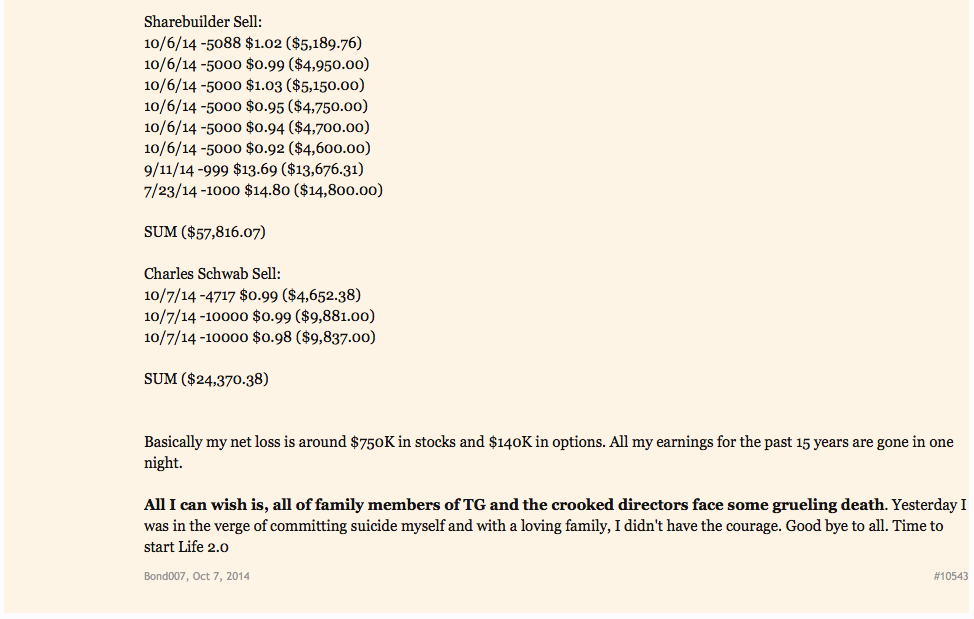

He later breaks down his losses, which amount to $750,000 in stock and $140,000 in options. Because he used borrowed money to fund part of the transactions, he not only lost everything, wiping out 15 years of savings, he owes his brokerage firm $107,000, which they are going to demand or else they’ll throw him into bankruptcy court.

We can reasonably surmise that his accounts held approximately $783,000 in fully-paid, non-borrowed assets. According to his profile, he is 44 years old. Even if he had never saved another penny in his life, at average rates of return, he could have retired at 65 with $5,000,000 to $6,000,000 in tax-sheltered assets. At that point, he could have rolled everything over to a self-directed IRA and used it to buy apartment or office buildings at a 10% cap rate (which are still very easy to find in much of the Midwest), living off between $500,000 and $600,000 in gross rents per year. There was no reason for this gamble. He had won. He could have spent every one of the rest of his paychecks for life on luxuries and still ended up okay. Yet, now he’s facing a very real probability of personal ruin because of a desire for more, quicker. It’s devastating.

Here’s another one … this guy not only went “totally” in on GTAT, but so did his wife and son!

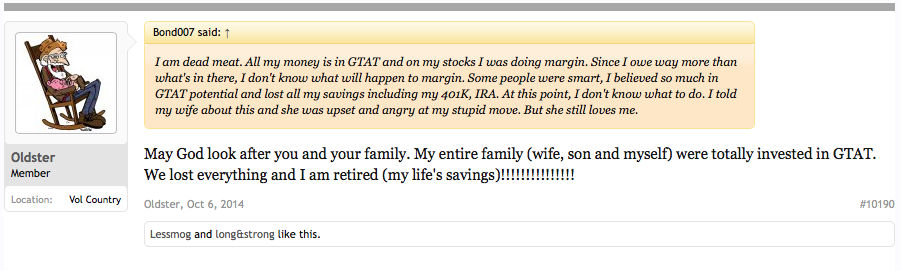

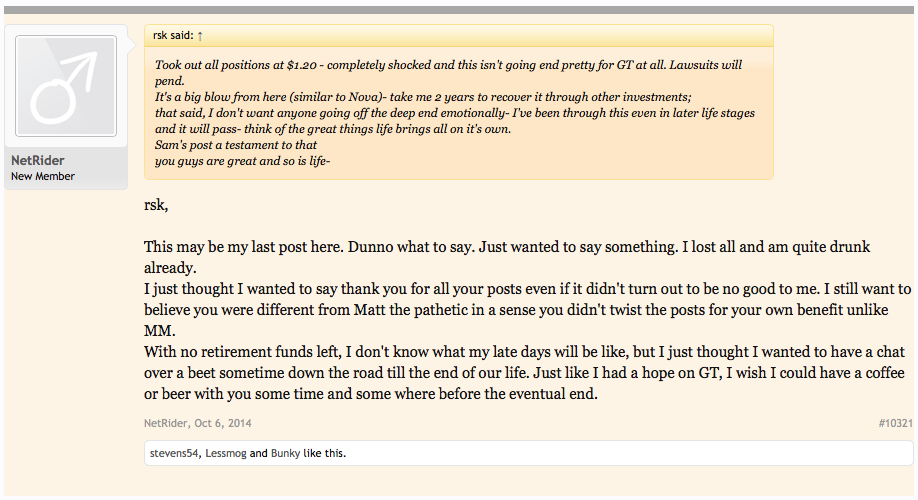

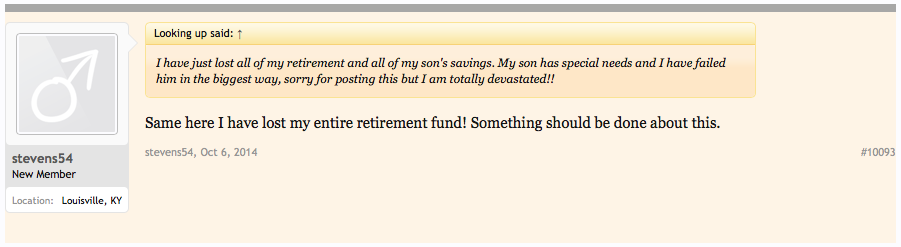

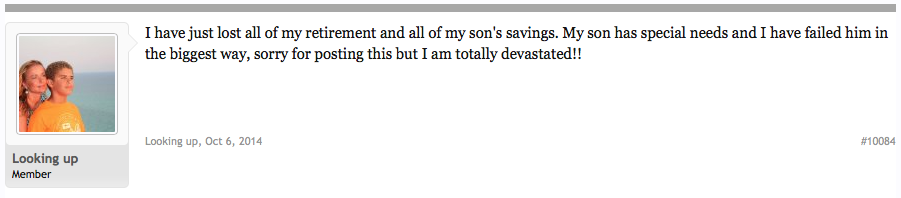

This person lost his or her entire retirement fund …

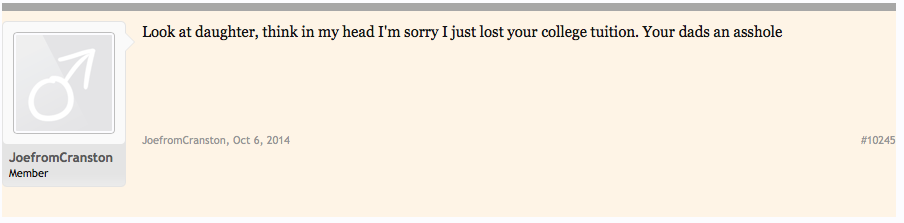

This father just lost his daughter’s college tuition …

This person is hiding the losses from his family …

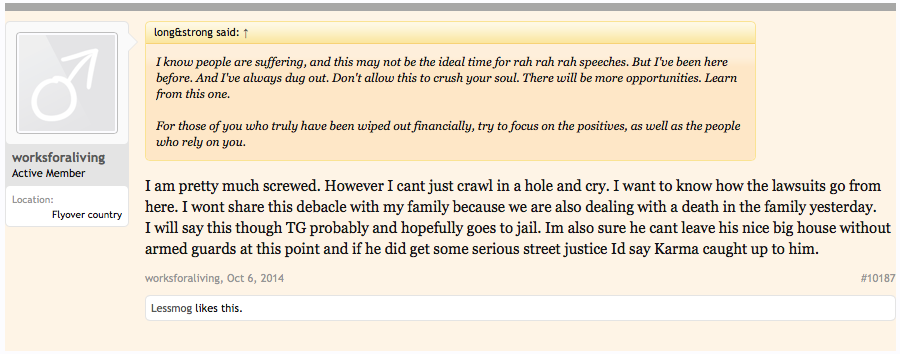

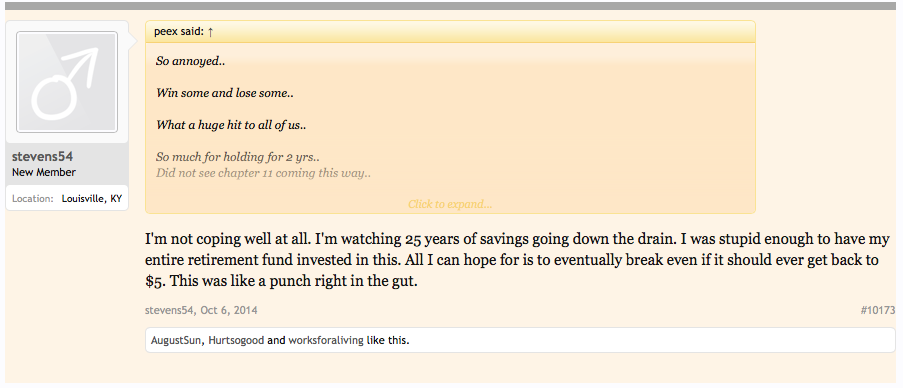

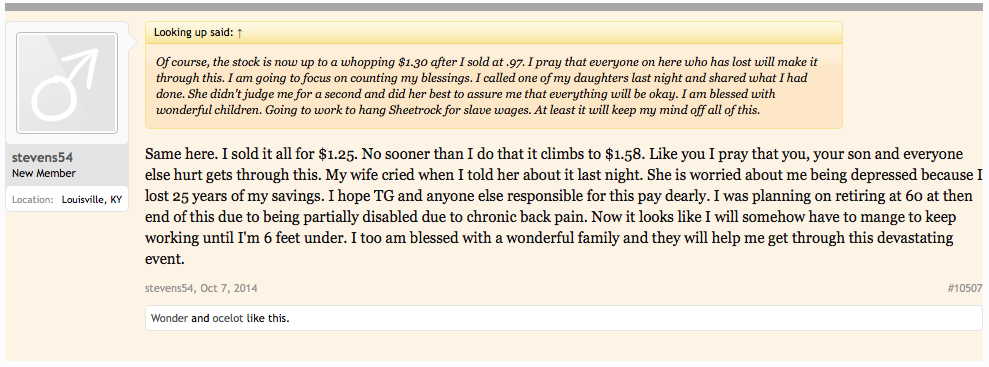

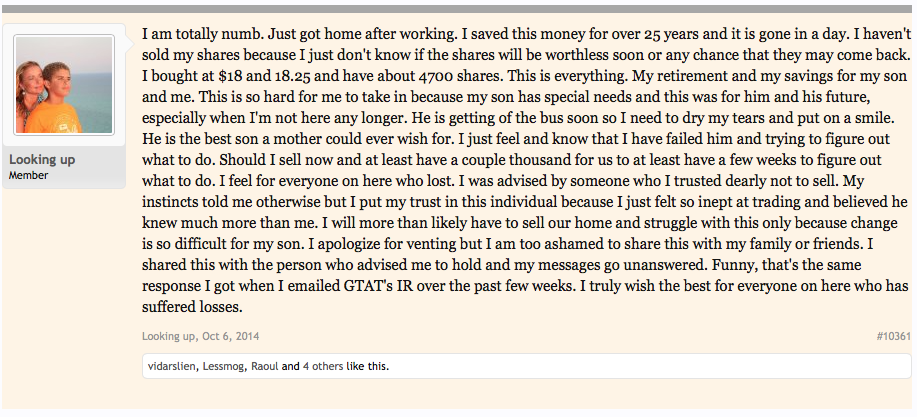

Another guy who lost his entire retirement account, 25 years of savings gone …

This woman is having to put her house on the market because she had taken her entire life’s savings and used them to buy 4,700 shares of the company, which she sold for next to nothing …

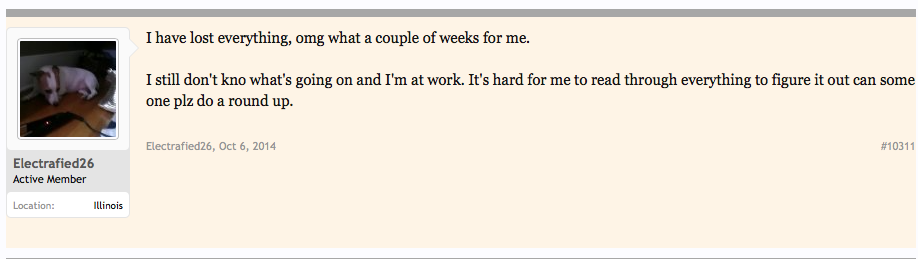

This person discovered he or she had lost everything while still at work …

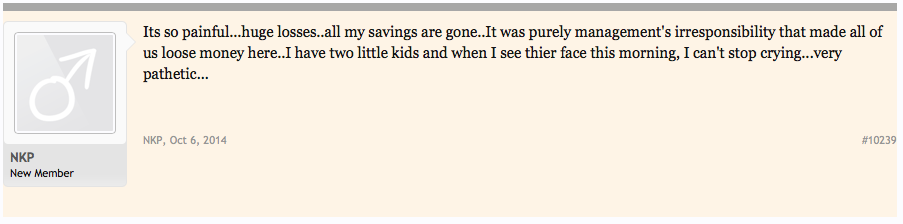

Another who lost all of his savings …

There are too many. You need to go read them for yourself. There is enough here, both in the GT Advanced Technologies filings and the forum response, to teach an entire semester course at university.

I’ve said it before, and I’ll say it again, but I think the do-it-yourself retirement system in the United States has been a social policy disaster. It works so well for rational, disciplined people. Meanwhile, others who work hard and are good folks but lack the temperament or experience to manage capital, lose everything. In the old days, everyone drew a pension check. I worry that as more and more of the country reaches retirement under the non-pension system, you’re going to have a very vocal minority of families screaming they can’t survive because they have no savings, no 401(k) funds … and somehow expect the government to pay their bills, which really means taxing everyone else who did behave responsibly even more to fund transfer payments; e.g., higher Social Security benefits. If this were 1970, none of these people would have had access to their retirement money in the first place. It would have been pooled, and managed, by the pension portfolio officers, who were bound under restrictive laws to put the cash to work in blue chip stocks and gilt-edged bonds at huge economies of scale. The workers never saw the pension plan assets fluctuating like crazy so they didn’t lose any sleep over the 1973-1974 stock market crash. It was a better system for most men and women, I think.

Just like Senator Roth introduced the Roth IRA, were I a Senator, my primary objective would be to introduce the Kennon Pension. I think it is possible to create mobile, portable pension plans that move from company-to-company with workers. It would take only a slight tweak to the tax code, and very draconian rules for financial institutions that offer them (e.g., maximum statutory limits on promised returns). You could make contributions and buy additional income for life. It’d be a superior system for a lot of people who would never have to worry about running out of money, while offering a huge new market for Wall Street. Annuities should fit the niche, in theory, but they fall short at present.